What the PMI Tells Us

The Purchasing Managers' Index is a monthly survey of procurement managers across Kenya's private sector. A reading above 50 indicates expansion; below 50 indicates contraction. Kenya's PMI dropped to 47.7 in March 2026 and has been below 50 for consecutive months, indicating sustained business contraction across manufacturing, services, and wholesale/retail sectors.

For supply chain professionals, the PMI is not an abstract economic indicator. It is a leading signal of operational conditions you will face in the coming months: which suppliers will remain viable, how procurement costs will move, and what demand patterns to expect.

5 Operational Implications

1. Supplier Financial Stress

In a contracting economy, your suppliers face the same pressures you do. Reduced order volumes, tighter credit, rising input costs. Some will cut corners on quality. Some will delay deliveries to manage cash flow. Some will go out of business without warning. Monitor your suppliers' financial health more closely during contraction periods. Request quarterly financial statements from critical suppliers. Watch for warning signs: delayed deliveries, quality inconsistencies, requests for advance payment, reduced communication.

2. Procurement Cost Volatility

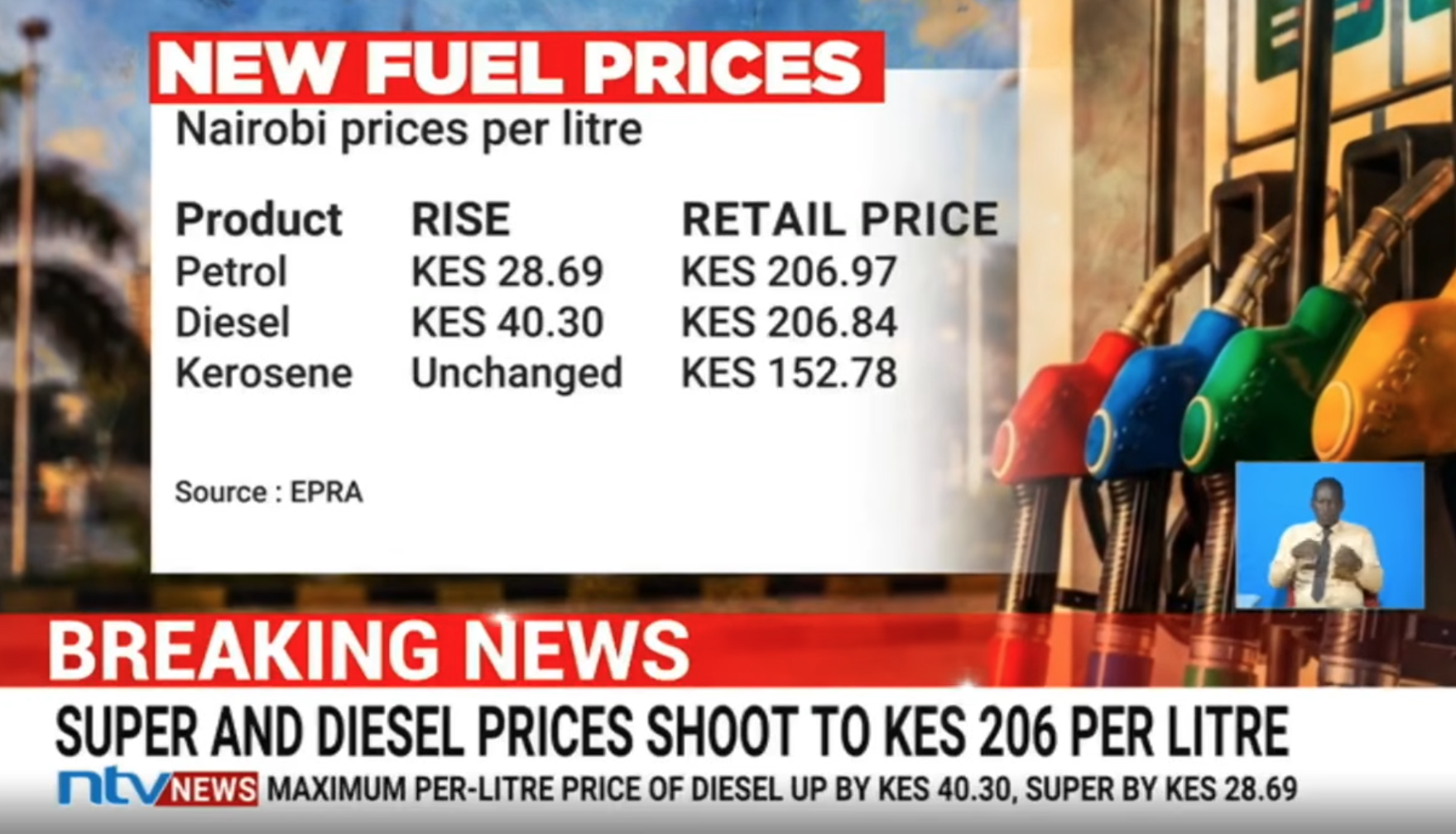

A contracting PMI often coincides with currency depreciation and input cost inflation. The Kenya shilling's performance against the dollar and euro directly affects import-dependent procurement costs. Budget for higher volatility. Build 10-15% contingency into procurement budgets for price movements. Lock in prices through framework agreements where possible.

3. Demand Uncertainty

Your own demand forecasts may become less reliable during economic contraction. Customer behaviour changes. Programme funding may be adjusted. Government budget allocations may be delayed or revised. Review demand forecasts monthly during contraction periods rather than quarterly.

4. Competitive Procurement Advantage

Contraction also creates opportunities. More suppliers competing for fewer orders means better pricing power for buyers. Negotiating leverage increases. This is a good time to renegotiate framework agreements, pre-qualify new suppliers (who may now be more willing to engage), and consolidate volumes for better terms.

5. Working Capital Pressure

Contraction tightens working capital across the economy. Payment cycles lengthen. Cash flow becomes constrained. Review your payment terms with both suppliers and customers. Consider offering faster payment in exchange for better pricing — your suppliers may value cash flow certainty more than margin during contraction.

What to Do This Month

Three immediate actions: (1) Conduct a supplier viability assessment — identify your most financially vulnerable critical suppliers and develop contingency plans. (2) Review your safety stock levels — contraction increases supply uncertainty. (3) Renegotiate at least one major contract — your negotiating position is stronger in a buyer's market.

Need a supply chain risk assessment in light of current economic conditions? Contact Us for a structured review.